Live retirement on your terms.

A majority of Americans age 65+ (70%) will need

some form of long-term care in their lifetimes.

Of that 70%, 1-in-5 will require

long-term care for more than 5 years.

(Source: “How Much Care Will You Need?” longtermcare.gov

U.S. Department of Health and Human Services – February 2017)

Asset Based Long Term Care

A possible solution for long term care expenses

Paying for long term care can be taxing on a retirement portfolio. In fact, in some ways it may be like creating a second, more expensive household.

Planning ahead for these expenses may make it possible to reduce your out of pocket expenses for long term care.

Click here or call us today at 866-271-0215 to learn more

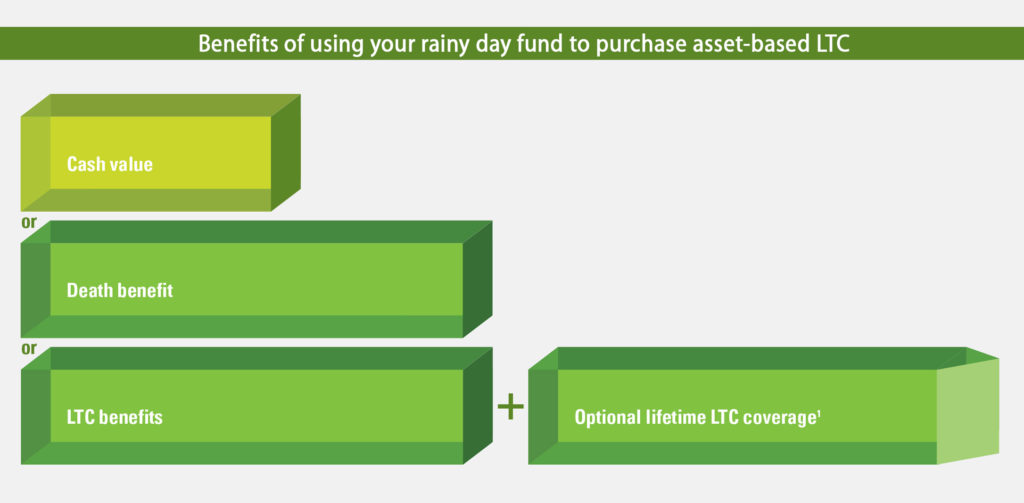

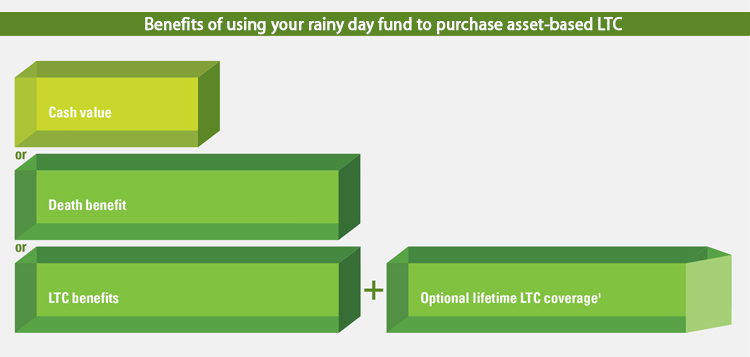

When you own asset-based long term care protection, you can be confident in 3 things:

• Your premium will never increase

• The amount of death/long term care benefits you have is guaranteed

• Your money earns interest with a minimum guaranteed interest rate

With Asset-Based care, there are two ways to pay for protection.

One option is to utilize an existing asset – typically money you currently have in CD’s, savings, annuities, IRA’s or retirement plan funds – as your guaranteed single premium.

A second option is to pay in a more traditional way, making annual premiums that are guaranteed to never increase.

Click here or call us today at 866-271-0215 to learn more

Addtional Information:

• Choice of assisted living, home health care, nursing home benefits and memory care

• Lifetime coverage is available through an optional rider (additional premium required)

• A way for one policy to cover an individual (single life) or both spouses (joint life)

Tax Information:

• LTC Benefits paid from asset-based long term care protection are income-tax free

• Interest accumulation is tax-deferred

• The life insurance benefit, if not used for LTC, is payable to your beneficiary, federal income-tax free

Products issued and underwritten by The State Life Insurance Company® (State Life), Indianapolis, IN, a OneAmerica company that offers the Care Solutions product suite. Not available in all states or may vary by state. Generally, riders may be optional and carry an additional cost. The long-term advantage of a rider will vary with the terms of the benefit and the length of time the product is owned. As a result, in some circumstances, the cost of a rider may exceed the actual benefit paid under that rider. Any individuals used in scenarios are fictitious and all numeric examples are hypothetical and were used for explanatory purposes only. All guarantees are subject to the claims-paying ability of State Life.